Hiroshi Ueda

- Classification

- Equity

- Company

- Spiritus Investments Co.,Ltd. (business closed)

Hiroshi Ueda established Spiritus Investments in February 2010 and has served as CIO since the foundation. Prior to Spiritus Investments, he was a Fund Manager of Morgan Stanley Asset & Investment Trust Management Co., Limited where he managed the Japanese Equity Growth strategy. He joined Morgan Stanley in 1996 and was responsible for newly constructing the investment strategy, launching the growth fund, researching companies, and building the portfolio. Prior to joining Morgan Stanley, he was a fund manager of Separate Account Management Department at Dai-ichi Mutual Life Insurance Company. During Dai-ichi Life, he was temporarily transferred to Fidelity Investments where he joined Earnings Growth Team led by Peter Lynch, which laid the foundation for his investment belief. He holds a B.A. in law from the University of Tokyo.

-

- Young companies at the stage of rapid growth in terms of sales and earnings. Characterized by small size and high-risk high-return investing.

-

- Focus on growth opportunities. Main driving force of performance at risk on environment

-

- Companies that preserves healthy earnings structure and sustainable earnings growth typically by securing a high share in niche market. Characterized by small size, low beta, and low risk.

- Focus on the degree of certainty about earnings growth. Performance driver at sluggish stock market.

Investment philosophy:

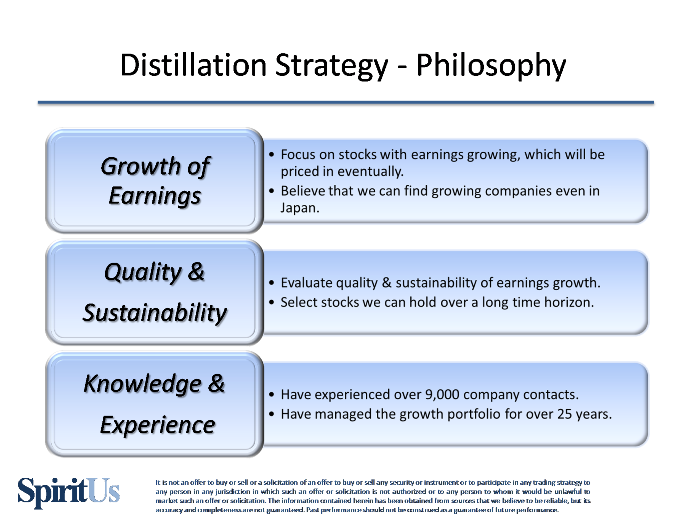

We seek to increase the share price of individual company from the earnings growth and pursue medium- and long-term returns by carefully selecting and investing stocks through evaluating the quality and sustainability of earnings growth.

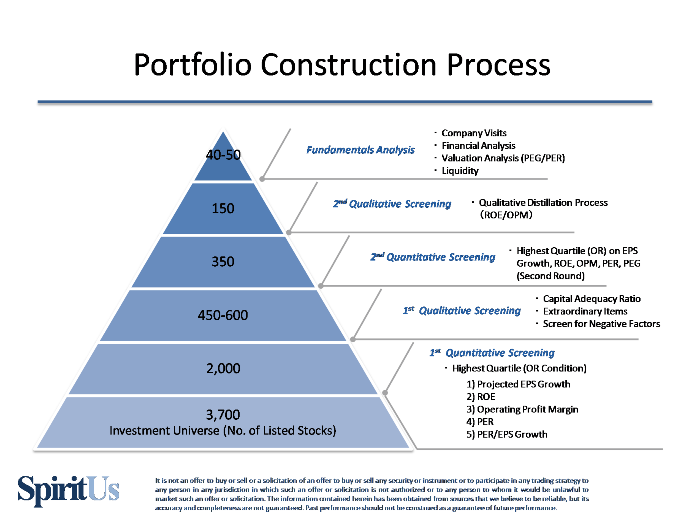

Investment process: (Please refer to the chart below.)

Regardless of whether market capitalization is large or small, we carefully select the stocks that can be possessed in the medium- to long-term from among all listed stocks. At the beginning, we narrow down candidate stocks by using a mechanical quantitative screening. We use (1) expected EPS growth rate, (2) ROE, (3) operating profit margin, (4) PER, and (5) PEG Ratio [= (4) divided by (1)]. These five are indicators to screen stocks with high-growth and high-quality of earnings as well as reasonable valuations. We exclude companies with capital adequacy ratio less than 10% and outliers, further investigate candidate stocks narrowed down by screening, and decide stocks to be invested. Needless to say, final fundamentals analysis is the most important process.

Looking at the Japanese stock market in terms of investment style, it was dominated by the growth over the last few years, but the value factor dominated for a long time since 1990. We believe that it is possible to outperform the market over the medium- to long-term by carefully selecting and investing growth stocks. I have own experience with growth-style for over 25 years, I think that there are enough opportunities for investing in promising growth stocks even in Japan where the declining birthrate, aging population, and the declining potential growth rate. For example, in the current portfolio, we hold a lot of domestic demand sectors such as services and retail trade. Looking at Japan as a whole, the growth rate of GDP declines, the domestic demand sector seems to be unattractive, but the size of Japan's economy itself is still the third-ranked in the world and we think that it is possible to find companies that can expand the market share. If a company can expand its market share in growing hot markets, the growth rate will be high. However, it will attract market attention, and consequently its valuations will be high. On the other hand, if we can find a company that can steadily increase its market share even in a mature or gradually decreasing market, we have opportunities for investing it in reasonable valuation as the market's attention is not so high. Meanwhile, companies steadily growing in overseas markets are of course promising, and we believe that we have sufficient opportunities for investing in companies that are called global niches that possess differentiated technologies and products in the manufacturing sectors.

For two years from April 1988, trainee experience at the Fidelity in Boston is a great starting point. I learned the bottom-up approach based on fundamentals analysis there, and have made it as a foundation for investing in Japanese equities. As for the investment style, I have been consistently based on the growth style, influenced by the "Earnings Growth" team led by Mr. Peter Lynch at Fidelity. I think that the real pleasure of the growth style investment I learned there has had a great influence on my own management style afterwards.

The key point is to do thoroughly the bottom-up approach. Since launching the current company, the number of in-house meetings and so on has decreased and the degree of freedom of the research activities has increased, and I have further raised the volume of corporate researches. At Spiritus, we have collected information through more than 4,000 company contacts over the past seven years, and especially over 1,000 IRs (including results meetings and small meetings) in 2016. I have a new appreciation for the fact that Mr. Peter Lynch of Fidelity held 1,400 stocks in his portfolio with AUM of 1.4 trillion yen at that time. By increasing the amount of company research, we can get various types of valuable information. For example, companies that seem to be completely unrelated to our holdings might be connected in the supply chain or competing companies, and it is possible to obtain useful both positive and negative information and to notice the changing point of the company and the industry to which the company belongs. (We call this `Investment Synapse`.) Also, by conducting a wide range of company researches, there is a merit that a bottom-up business confidence different from top-down macro analysis can be fostered. Although we screen out companies in our investment process in order to increase research efficiency, we still have a lot of investment opportunities, which can be found in various fields and change with the times. We should always be free from prejudice and keep ourselves open to new ideas.

What I am trying not to do is not to invest in stocks that I cannot fully understand. For example, I invest in only one stock that I was convinced in biotechnology sector after investigating as many bio-related stocks as possible. In other words, we invest in stocks that we can explain easily with our own words to people who do not know the stock.

By raising the accuracy of stock selection, it is possible to limit the risk of declining individual stock and consequently the entire portfolio. Although our investment strategy is long-only, we pursue absolute returns over the medium- to long?term horizon. About 70% of the portfolio is constructed with stocks that maintain high profitability in niche markets, and such stocks have relatively limited downside risk when the market plummets. Indeed, even after the launch of Spiritus, the portfolio showed lower downside risk at the time of external shocks such as the Great East Japan Earthquake.

"One Up On Wall Street: How To Use What You Already Know To Make Money In The Market " by Peter Lynch I read it in the Fidelity training days and laid my first foundation as a fund manager. It is an easy-to-understand basic book as well as a great reference that average investors should keep in mind. Mr. Peter Lynch is a great fund manager who directly advised me of the attitude as a fund manager at Fidelity in Boston.

If it comes to checking everyday it will be the Nikkei Newspaper. Since our company research is the basis for our investment, we place great importance on information available from companies. It is also important task for me to check the earnings results of companies that are announced day-to-day.

Notes:

This article originally appeared on March 1, 2017. Any views presented in this article are as of such date and are subject to change.

This article and the information provided therein are not a recommendation to purchase or sell any security, nor are they intended to constitute the marketing of, or a solicitation for investment in, any investment product.

Spiritus Investments is an independent, boutique investment advisory firm founded in February 2010 by Hiroshi Ueda and Yoshihiko Ochiai to specialize in Japanese growth equity investment management. The firm has provided investment advice relating Japanese equity for pension funds and a fund wrap since June 2010.

Previously, the founders worked at Morgan Stanley Asset & Investment Trust Management Co., Limited. Hiroshi Ueda, portfolio manager, has experienced over 9,000 company contacts and has managed the growth portfolio for more than 25 years.

The firm has advisory license in Japan and membership of Japan Investment Advisers Association.

We focus on Japanese stocks with earnings growing, which will be priced in eventually. And we believe that we can find growing companies even in the mature Japanese market. Through significant knowledge and experience, we evaluate quality and sustainability of earnings growth, and select stocks we can hold over a long time horizon.

We place an emphasis on the following two growth categories.

(1) Emerging Growth

(2)Earnings Quality

March 1, 2017

by Investment in Japan